The state of restaking in 2026

Restaking has transitioned from a speculative experiment into a foundational layer for Ethereum's infrastructure. What began as a novel way to reuse staked ETH now underpins a growing ecosystem of Actively Validated Services (AVS) and Layer 2 networks. This shift marks a move from isolated yield generation to a shared security model that supports the broader network.

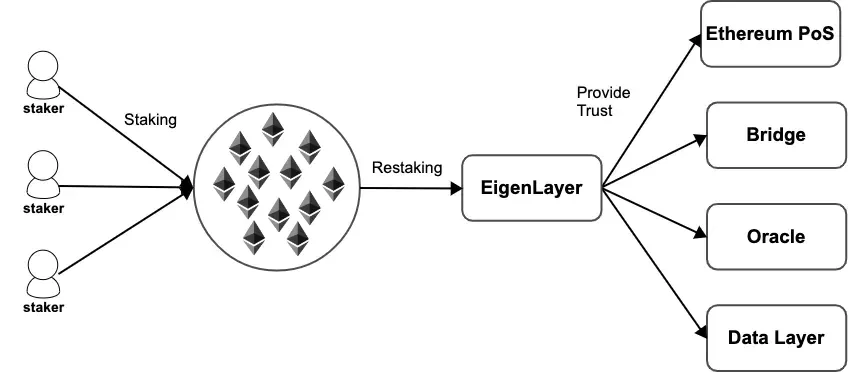

The primary driver of this maturity is EigenLayer's AVS framework. By allowing operators to delegate their staked ETH to new services, the protocol has created a marketplace for security. This mechanism enables L2s and other infrastructure projects to borrow security rather than building their own validator sets from scratch, reducing fragmentation and enhancing overall network resilience.

The integration of restaking into L2 synergy is becoming increasingly critical. As Layer 2 solutions scale, they rely on the underlying security of the Ethereum mainnet. Restaking provides a flexible way to align incentives between L2 operators and Ethereum stakers, creating a more cohesive ecosystem. This interdependence suggests that restaking is no longer optional but a strategic necessity for sustainable scaling.

While the potential for yield remains attractive, the focus in 2026 is on stability and utility. The market is moving away from high-risk, high-reward narratives toward sustainable infrastructure. This cautious approach ensures that restaking contributes to the long-term health of the Ethereum ecosystem rather than introducing systemic risks.

EigenLayer AVS adoption metrics

Active Verification Services (AVSs) are moving from experimental testnets to core infrastructure for Layer 2s and DeFi protocols. The primary driver is the ability to outsource specialized security tasks—such as data availability checks, oracle verification, and cross-chain message validation—to EigenLayer’s shared security pool. This shift allows protocols to access institutional-grade security without building and maintaining independent validator sets.

Adoption is accelerating as protocols seek to reduce the capital expenditure required for bootstrapping security. By leveraging restaked ETH, projects can secure their services at a fraction of the cost of launching a new consensus layer. This model is particularly attractive for data availability layers and optimistic rollups, which require constant, low-latency verification that is expensive to maintain independently.

The market is responding to this utility. Restaking yields have adjusted to reflect the risk premiums of specific AVSs, creating a more granular yield environment. Investors are no longer just earning a base staking rate; they are pricing in the specific security guarantees provided by each service. This has led to a more efficient capital allocation, where high-security needs command higher yields.

The integration of AVSs into L2 ecosystems is creating a synergistic effect. As L2s adopt EigenLayer for security, they contribute to the overall robustness of the Ethereum ecosystem. This creates a feedback loop: more security attracts more developers, which increases the value of the underlying asset, which in turn supports higher staking yields. This dynamic is reshaping the competitive landscape, favoring protocols that can effectively integrate shared security services.

Layer 2 restaking strategies compared

Restaking on Layer 2s introduces distinct risk and yield profiles depending on the underlying asset and the specific Active Verification Service (AVS) architecture. While base Ethereum staking yields hover around 2.78% APR, with MEV-Boost adding 0.5–1% for validators, L2 strategies often decouple from these baseline metrics to offer higher, albeit riskier, returns. The choice of strategy hinges on whether you prioritize capital preservation through native ETH exposure or seek yield augmentation via LST derivatives and L2-specific liquidity provisions.

The following comparison outlines the primary trade-offs between native ETH restaking, Liquid Staking Token (LST) restaking, and L2-native strategies. Each approach carries unique liquidity constraints and smart contract risk exposures that must be weighed against potential APR enhancements.

| Strategy | Yield Source | Risk Profile | Liquidity Terms |

|---|---|---|---|

| Native ETH Restaking | Base APR (~2.78%) + MEV | Low to Moderate | Locked during validator exit |

| LST Restaking | Staking APR + LST derivatives | Moderate (Smart Contract + DeFi) | High (Tradable on DEXs) |

| L2-Specific AVS | AVS incentives + Base Yield | High (New AVS Risk) | Variable (Protocol Dependent) |

Native ETH restaking remains the conservative anchor for most portfolios. By restaking directly on EigenLayer or similar protocols using staked ETH, participants retain the security of the base layer while earning additional AVS incentives. The primary constraint is liquidity; funds remain locked until the validator exit queue clears, a process that can take weeks or months depending on network congestion. This strategy minimizes exposure to liquid staking derivative (LSD) protocol risks but sacrifices immediate capital flexibility.

LST restaking offers greater liquidity by allowing users to restake tokens like rETH or stETH. This approach integrates DeFi composability, enabling users to earn yield from restaking while still utilizing their tokens in lending markets or liquidity pools. However, it introduces a layered risk profile: users are exposed to both the underlying staking protocol and the LST provider’s smart contract integrity. The yield potential is often higher due to the ability to capture both staking rewards and DeFi yield, but the complexity increases the attack surface for exploits.

L2-specific restaking strategies are emerging as a high-risk, high-reward frontier. These protocols often offer significant incentive programs to bootstrap liquidity and secure new AVSs. While the APRs can be substantially higher than base Ethereum yields, the risk of smart contract vulnerabilities in newer L2-specific implementations is elevated. Additionally, liquidity can be fragmented across different L2 bridges and protocols, potentially complicating exit strategies. Investors should approach these opportunities with caution, verifying the audit status and track record of the specific AVS before committing capital.

Yield compression and risk factors

Restaking is no longer a simple yield booster; it has become a complex financial instrument where returns are actively compressed by market saturation and operational overhead. As EigenLayer and other Actively Validated Services (AVS) mature, the easy alpha of early adoption has faded. In 2026, the base yield for Ethereum staking sits at roughly 2.78% APR, with MEV rewards adding another 0.5–1% for validators running MEV-Boost. For restakers, these base rates are further diluted by AVS-specific fees and the cost of securing additional services, leading to a net yield that often barely outpaces inflation when risk is accounted for.

The primary risk in this environment is not just market volatility, but the structural complexity of multi-layered staking. Each additional layer of security introduces new attack surfaces and operational dependencies. A failure in a downstream AVS or a misconfiguration in the restaking contract can lead to slashing events that penalize the entire restaked position, not just the isolated service. This interconnectedness means that a local failure can cascade, turning a minor technical glitch into a significant capital loss.

Callout: Higher yields in restaking often correlate with higher operational complexity and slashing risk. Delegators must understand that the "premium" yield is compensation for taking on the risk of validator misbehavior across multiple protocols.

MEV (Maximum Extractable Value) plays a dual role in this dynamic. While it provides a vital revenue supplement for validators, it also introduces censorship and centralization risks. As MEV-Boost and related protocols become more sophisticated, the distribution of MEV rewards becomes less uniform, favoring large operators with superior infrastructure. For smaller restakers, the marginal gain from MEV may not justify the increased exposure to potential slashing penalties associated with participating in complex MEV pipelines.

The landscape is further complicated by emerging risks in other ecosystems. Solana, for instance, plans to enable slashing by 2026, introducing new risk parameters for delegators who may consider cross-chain restaking strategies. As the industry moves toward a multi-chain restaking future, the lack of standardized security audits and interoperability protocols means that risk assessment must be rigorous and continuous. Investors should view restaking not as a passive income stream, but as an active management task requiring constant monitoring of protocol health and validator performance.

No comments yet. Be the first to share your thoughts!