Restaking 2026: The Shift to Shared Security

The narrative around restaking has matured from speculative hype to functional infrastructure. In 2026, the focus has shifted from marketing promises to the stable deployment of shared security protocols. EigenLayer, the dominant force in this space, has stabilized with a total value locked (TVL) consistently exceeding $15 billion, signaling institutional confidence in the model's durability rather than short-term yield chasing.

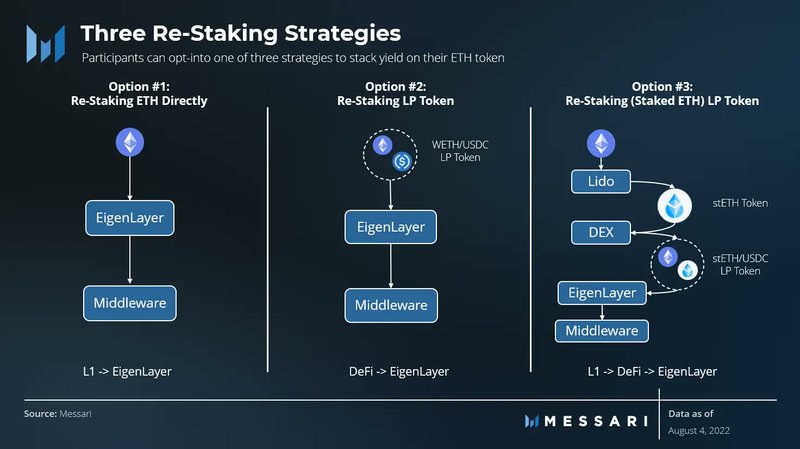

At its core, restaking allows staked ETH to secure not just the Ethereum base layer, but also Actively Validated Services (AVSs). This creates a "security marketplace" where validators can delegate their existing staking power to new networks. The result is a multi-layer yield engine: validators earn base staking rewards, restaking fees, and additional AVS incentives simultaneously. This structure transforms previously idle or single-purpose capital into a versatile resource for the broader ecosystem.

However, this efficiency comes with complex risk vectors. The primary concern is "slashing"—the penalty for malicious behavior. In a shared security model, a validator's entire restaked balance can be at risk if they fail to perform correctly across multiple AVSs. This amplifies the cost of failure, requiring validators to maintain rigorous operational standards. The infrastructure is no longer experimental; it is a high-stakes financial layer where security is a shared, yet potentially concentrated, liability.

EigenLayer V2: Upgrading the Restaking Core

The initial launch of EigenLayer established the foundational model for restaking, allowing Ethereum stakers to delegate their security to multiple Actively Validated Services (AVSs). While this innovation unlocked new yield opportunities, it also introduced significant systemic risks. The protocol’s early architecture relied heavily on a small number of large operators and lacked granular control over slashing conditions, creating a single point of failure that threatened the entire ecosystem. EigenLayer V2 addresses these structural vulnerabilities through a more robust, decentralized framework designed to mitigate cascading failures.

A primary upgrade in V2 is the implementation of improved slashing conditions and operator diversity requirements. In the original launch, slashing penalties were often binary and blunt, punishing operators for failures across any service they supported, which discouraged participation from smaller, more agile validators. V2 introduces a more nuanced slashing mechanism that allows for service-specific penalties. This means an operator can be penalized for failing to secure one AVS without necessarily losing their entire stake or being slashed for unrelated services. This granularity encourages a more diverse operator set, reducing the concentration of power among a few dominant entities.

The economic model has also been refined to better align incentives between restakers, operators, and AVS providers. V2 introduces a more sophisticated fee distribution system that accounts for the varying levels of security provided by different services. This ensures that operators are compensated fairly for the additional computational and security burdens they take on, while restakers can choose services that match their risk tolerance. The protocol also enhances transparency by providing real-time data on operator performance and slashing events, allowing market participants to make more informed decisions.

These technical upgrades are not merely incremental improvements; they represent a fundamental shift in how restaking security is managed. By decentralizing operator power and refining slashing conditions, V2 creates a more sustainable environment for long-term growth. The protocol’s ability to adapt to these early challenges demonstrates its commitment to building a secure, scalable infrastructure for the broader Ethereum ecosystem. As the restaking landscape continues to evolve, V2’s framework will likely serve as the standard for future security layer implementations.

Top Liquid Restaking Tokens Compared

Liquid Restaking Tokens (LRTs) have evolved from simple ETH wrappers into distinct protocols with different risk profiles and yield structures. In the 2026 landscape, choosing an LRT is no longer just about picking the highest Annual Percentage Yield (APY); it is about selecting a security model that aligns with your tolerance for smart contract risk and slashing exposure.

The following comparison focuses on structural differences between leading protocols like Renzo, Kelp DAO, and Puffer. These platforms manage restaked assets through varying degrees of decentralization and insurance mechanisms. While yields fluctuate with network activity and EigenLayer rewards, the underlying architecture determines how capital is protected during market stress.

Protocol Comparison

| Protocol | Primary Asset | Yield Source | Security Model |

|---|---|---|---|

| Renzo (ezETH) | ETH | Restaking rewards + Liquidity incentives | Community-governed insurance fund |

| Kelp DAO (rsETH) | ETH | EigenLayer AVS rewards | Decentralized validator network |

| Puffer (pufETH) | ETH | Restaking + MEV | Staking-as-a-service infrastructure |

| Swell (swETH) | ETH | Restaking + Liquid staking | Early mover, high liquidity focus |

Key Structural Differences

Renzo emphasizes community ownership through its insurance fund, which is designed to cover potential slashing events. This model appeals to users seeking a safety net beyond the protocol's smart contracts. Kelp DAO relies on a decentralized network of operators, distributing risk across a broader set of validators. Puffer operates more like a staking-as-a-service provider, leveraging institutional-grade infrastructure to minimize downtime and optimize MEV capture.

Swell remains a dominant player due to its early market entry and deep liquidity. However, newer entrants often offer higher incentives to attract capital, creating a dynamic where yield is frequently subsidized by protocol token emissions. Readers should distinguish between sustainable restaking rewards and temporary emission incentives.

Evaluating Risk and Yield

When comparing these tokens, look beyond the headline APY. The "yield" often consists of two parts: base ETH staking rewards and additional incentives from the LRT protocol itself. The latter can be volatile and may decrease as the protocol matures. Additionally, consider the smart contract risk associated with each LRT's bridge and vault mechanisms.

For real-time performance data, refer to the ETH price chart below to contextualize restaking returns against the underlying asset's performance.

How Yields Are Generated

In 2026, yield from restaking is no longer a single stream but a layered aggregation of distinct economic activities. When you restake ETH or SOL through EigenLayer or Jito, you are not merely earning the base staking reward. You are leasing your security to Actively Validated Services (AVSs) that require consensus power to operate.

The primary yield component remains the native validator reward, typically 3-5% for ETH. The secondary layer comes from AVS fees. These are payments made by services like decentralized oracle networks, data availability layers, or MEV-boosting relayers to secure their infrastructure. The final layer often involves liquid restaking token (LRT) incentives, where protocols distribute additional tokens to bootstrap liquidity and network participation.

This structure creates a composite yield that is significantly higher than traditional staking. However, the complexity of these layers means that returns are variable. A drop in AVS demand or a reduction in LRT incentives can cause the total yield to fluctuate, often tracking the broader crypto market rather than offering a fixed income.

Understanding Slashing and Correlation Risks

The higher yields come with structural risks that do not exist in simple staking. The most immediate threat is slashing. If a validator operator misbehaves—by signing conflicting blocks or going offline—the protocol can confiscate a portion of the staked capital. In a restaking environment, this risk is amplified because your capital is secured across multiple AVSs. A single misconfiguration can trigger penalties across all services you are secured for.

Correlation risk is the second major concern. In 2026, the majority of restaking protocols are built on Ethereum. If the Ethereum network experiences a significant outage or a major exploit in a foundational AVS, the entire restaking ecosystem can suffer simultaneously. This is not a diversification benefit; it is a concentration of risk. Your assets are exposed to the same underlying settlement layer, meaning a systemic failure on Ethereum impacts all restaked positions.

Managing these risks requires active monitoring. Unlike passive staking, restaking demands that you understand the specific security assumptions of each AVS you support. Ignoring these nuances can lead to significant capital loss, making education and careful selection of operators essential for sustainable returns.

No comments yet. Be the first to share your thoughts!