Restaking 2026: The Shared Security Shift

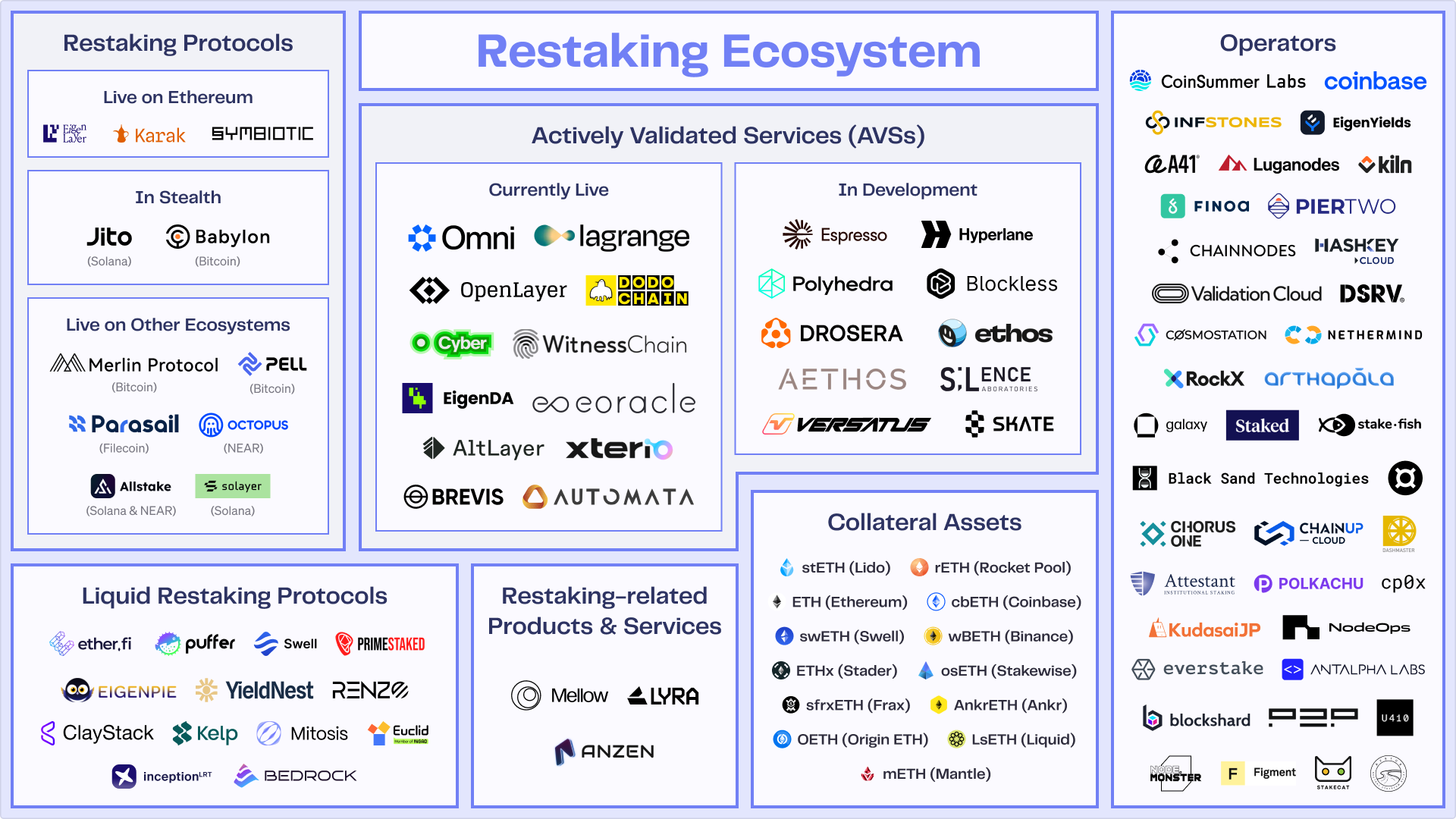

Restaking has evolved from a novel Ethereum experiment into the foundational layer of decentralized security. At its core, restaking allows stakers to reuse their already-staked ETH to secure additional decentralized protocols. This mechanism, often called shared security, creates a multi-layered defense where a single validator’s stake protects not just the Ethereum mainnet, but also oracles, bridges, and rollups.

In 2026, the market has shifted from experimental deployments to institutional-grade infrastructure. The early days were defined by high-yield speculation and fragmented liquidity. Today, the focus is on robust risk management, standardized interfaces, and sustainable yield models. EigenLayer V2 and Liquid Restaking Tokens (LRTs) have matured, offering clearer risk boundaries and better capital efficiency. This maturation reduces the systemic risks that plagued earlier iterations, making restaking a viable option for conservative capital allocators.

The economic logic remains simple but powerful: validators provide security, and protocols pay for it. However, the complexity lies in the delegation. Restakers must carefully select which services to secure, balancing potential rewards against the risk of slashing. This choice transforms ETH from a passive yield asset into an active security provider.

To understand the current baseline, it helps to look at Ethereum’s price action alongside staking metrics. A strong ETH price supports healthy staking participation, which in turn stabilizes the restaking ecosystem.

This shift toward shared security represents a critical upgrade for the broader crypto economy. By pooling security, protocols can launch with less capital while maintaining high levels of decentralization. For validators, it offers a new revenue stream that complements traditional staking rewards. As the technology stabilizes, restaking is becoming less of a speculative gamble and more of a standard utility in the digital asset landscape.

EigenLayer V2 and Protocol Upgrades

EigenLayer V2 introduces structural changes to how restaked capital is allocated and secured. The upgrade shifts the protocol from a passive security layer to an active governance engine, allowing validators to participate more directly in the economic incentives of Actively Validated Services (AVSs). This move addresses earlier criticisms that restakers were merely earning yield without contributing to network health or security audits.

The core technical improvement lies in the introduction of dynamic slashing conditions. Previously, slashing was triggered only by severe protocol failures. V2 enables AVSs to define custom slashing criteria, allowing them to penalize validators for downtime, latency, or other performance metrics relevant to their specific service. This creates a tighter coupling between security provision and service quality.

Liquidity remains a primary concern. The upgrade includes mechanisms to improve the composability of restaked assets, reducing the fragmentation that often occurs when the same ETH is secured across multiple AVSs. By standardizing how liquidity is tracked and reported, EigenLayer V2 aims to prevent the over-collateralization issues that plagued early restaking models.

The economic model also evolves to better align incentives. Validators now face a more transparent risk-reward profile, with clearer visibility into potential slashing events and corresponding rewards. This transparency is critical for institutional participants who require predictable risk parameters before committing significant capital to restaking strategies.

Top Liquid Restaking Tokens Compared

The liquid restaking token (LRT) market has consolidated around three primary protocols: Ether.fi, Renzo, and Kelp. Each offers a distinct approach to securing EigenLayer AVSs while providing yield. Evaluating these options requires looking beyond headline APY to understand how each protocol manages risk, TVL concentration, and ecosystem integration.

| Protocol | TVL Rank | Yield Source | Risk Profile | Ecosystem |

|---|---|---|---|---|

| Ether.fi | 1 | EIGEN Staking + AVS | Lower (Diversified Ecosystem) | Native EigenLayer |

| Renzo | 2 | EIGEN Staking + Restaking | Medium (Active Management) | Cross-Chain (Multi-Chain) |

| Kelp | 3 | EIGEN Staking + AVS | Medium (High AVS Exposure) | EigenLayer + Gnosis |

Ether.fi leads in total value locked, leveraging its first-mover advantage to build a broad ecosystem of native restaking points. Its risk profile is considered lower due to the diversification across multiple AVSs and its native ETH (eETH) token which serves as a foundational liquidity layer.

Renzo differentiates itself through active management and cross-chain accessibility. By optimizing for yield across various restaking opportunities, it appeals to users seeking higher returns, though this active management introduces a slightly higher operational risk profile compared to passive protocols.

Kelp focuses heavily on AVS integration, particularly within the Gnosis ecosystem. While this offers high yield potential, it concentrates risk on specific AVS performance and security assumptions. Investors must weigh the higher potential rewards against the concentrated exposure.

Evaluating Restaking Risks and Rewards

Restaking introduces a layered security model where Ethereum validators contribute their stake to secure multiple protocols simultaneously. This amplification of yield comes with a proportional increase in exposure. When you restake, you are not just securing the base layer; you are extending your economic commitment to Actively Validated Services (AVSs). If any of these downstream protocols fail or violate their consensus rules, your underlying ETH is at risk.

The most immediate threat is slashing. In a standard staking arrangement, slashing occurs only if the validator misbehaves on Ethereum. With restaking, the risk expands. If a restaking operator or the underlying AVS violates its specific smart contract logic, the restaking protocol may enforce penalties against your staked assets. This means your capital is exposed to the operational integrity of multiple, often less battle-tested, smart contracts.

Liquidity and complexity add further layers of risk. Liquid Restaking Tokens (LRTs) offer flexibility but introduce custodial and smart contract risks. If the LRT protocol suffers a hack or a governance failure, the value of your tokenized stake can collapse independently of Ethereum’s performance. Additionally, the exit queues for unstaking can be lengthy during periods of network stress, potentially locking up capital when liquidity is most needed.

Despite these risks, the economic incentives remain compelling for those who understand the mechanics. The rewards from AVSs can significantly boost Annual Percentage Yields (APYs) compared to native staking. However, this is not free money. It is compensation for taking on counterparty and smart contract risk. Investors must weigh the potential yield against the possibility of slashing events, protocol exploits, and illiquidity during market downturns.

Ultimately, restaking is a high-stakes allocation. It suits operators who can actively monitor their AVSs and understand the specific slashing conditions of each service. For passive investors, the complexity and concentrated risk may outweigh the marginal yield gains, especially given the evolving regulatory and technical landscape of EigenLayer V2 and other restaking frameworks.

Restaking 2026: Checklist for Stakers

Entering the restaking ecosystem requires more than just locking ETH. You are providing security to Active Validator Sets (AVSs), which introduces new smart contract and slashing risks. Treat this as a capital allocation decision, not a passive yield farm.

Choose an LRT provider with audited smart contracts and transparent operator delegations. Look for protocols that have undergone formal verification and have a clear track record of handling slashing events. Avoid newer, unaudited pools that promise disproportionately high yields.

Not all AVSs carry the same risk. Evaluate the specific services your restaked capital secures. Some AVSs may involve complex oracle networks or bridge mechanisms that increase exposure to smart contract vulnerabilities. Stick to established AVSs with proven utility and lower technical complexity.

Slashing can result in the loss of your staked principal. Understand the conditions under which your validator could be penalized. Set up alerts for operator behavior and network health. Regularly review the governance proposals of your chosen LRT to ensure your capital remains aligned with your risk tolerance.

No comments yet. Be the first to share your thoughts!